On June 1, 2010, all Medigap plans were substantially changed. Some were eliminated, some were added, and most of the existing plans were modified. Two new Medicare Supplement Plans (M and N) were added, and one of the two plans – Medicare Supplement Plan N – was very popular. Recent developments, however, may change this assessment. Here are lessons learned from the Medigap Plan N story.

Medigap Plan N Basics

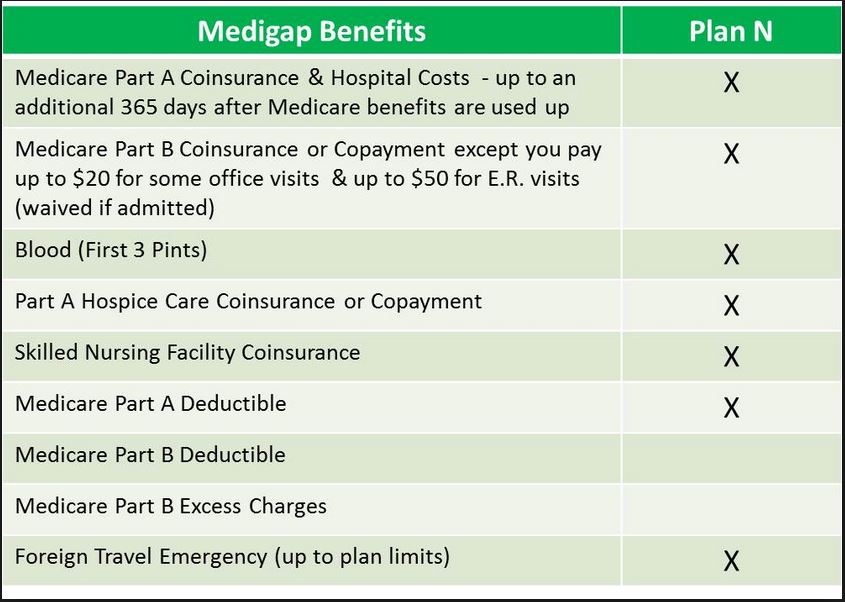

Medicare Supplement Plan N provides cost-sharing features with lower premiums than standard plans, such as Medigap plans F and G. Its cost is about 45% of Medicare Supplement Plan F’s cost. Medigap Plan N is as good as the Medigap Plan F, except:

- It does not pay the Part B Annual Deductible

- It does not pay Part B Excess Charges

- It pays 100% of the Part B coinsurance except for up to $20 copayment for office visits and up to $50 copayments for emergency department visits

In other words, the most critical Medigap benefits (Part A coinsurance and deductible and Part B coinsurance) are fully covered with $20/$50 copayments as described above. These copayments result in substantial Medicare Supplement Plan N premium savings compared with other Medicare Supplement plans.

When Medigap Plan N is a good value

Medigap Plan N is a good value for anyone in good health which only visits the doctor occasionally and doesn’t want to be “over-insured.”

- It may benefit the person who has Original Medicare and is ready to enroll in a Medicare Supplement Plan to cover what Medicare does not pay (i.e., 20% of the original bill without a maximum limit).

- Alternatively, it may be a good value for those enrolled in an expensive Medigap Plan and are considering switching to the more affordable Medicare Supplement Plan N.

It is worth emphasizing again that it does not pay to save a few hundred dollars in premium if you are is visiting doctors quite often (let’s say twice a month) and is paying the Medicare Supplement Plan N copayment – $20 – for each visit.

For those who are enrolled in Medicare Advantage and would like to return to Original Medicare, the affordable Medigap Plan N (compared with Plans C or F) may be an attractive option. No more network restrictions and superior coverage – not bad for an affordable premium with small copayments.

Sounds good right?

Guaranteed Issue (GI) and Medicare Supplement Plan N

To enroll as many clients as possible in Medicare Supplement Plan N, some insurance companies softened their Medical Underwriting Guidelines for Plan N. The most radical step was taken by the Mutual of Omaha insurance company (MOO). In all states where MOO sells Medicare Supplement Plans, Plan N was a virtually Guaranteed Issue (GI): it either asked no health questions at all or only asked about End Stage Renal Disease (ESRD). Unless someone has kidney failure, they will always pass the examination; so there were virtually no medical underwriting and almost no one could be denied coverage.

Usually, when someone applied for a Medigap policy, insurance companies used medical underwriting to allow them to screen potential applicants. The Medicare Supplement Open Enrollment Period (which runs for six months after getting Part B) is the exception to medical underwriting. This period is GI – during this time you cannot be denied coverage for any Medigap plan the insurance company provides.

The Medigap Plan N Story – GI Consequences

By making Medicare Supplement Plan N also a Guaranteed Issue, Mutual of Omaha attracted anyone who had previously been declined for other Medigap Plans because of medical underwriting either with Mutual of Omaha or with other insurance companies. The number of applicants for Plan N skyrocketed.

According to Mark Farrah, Associates Medicare Supplement market study: “As of the end of 2010, Medicare Supplement plans covered approximately 9 million seniors, with 44% choosing Plan F; and 147,912 choosing Plan N since it was released in June 2010… Mutual of Omaha ranked second in Medicare Supplement Market share with 11% share, rising from 8% in 2009”.

Of course, people in poor health flocked to MOO’s Medicare Supplement Plan N – it was their only opportunity to enroll in a Medigap plan. Unfortunately, some people with perfectly good health (who could pass medical underwriting) joined the MOO Plan N also.

MOO never promised that Medicare Supplement Plan N would stay GI forever. Realizing that it was not the smartest business move, MOO first switched on February 2011 from GI to a liberal (compared with other plans) medical underwriting policy and then discontinued Medicare Supplement Plan N altogether in ALL States in May 2011. The bubble burst. Plan N in MOO only lasted a short time – from June 2010 through May 2011. This was a sad conclusion of the Medigap Plan N story.

The Medigap Plan N Story – The Next Step

According to MOO press-release “Existing Plan N clients may keep their policy or replace it anytime with another Medicare Supplement we offer in the state. Normal conversion and underwriting rules apply.” Very substantial premium increases for the Medigap Plan N followed. Those people who are unable to pass underwriting with other plans/ insurance companies will probably stay with MOO’s Plan N (despite the more substantial premiums), or they may leave Medigap altogether and stay on Original Medicare only.

For everybody else who can pass medical underwriting, the best likely option is to switch to another plan and to do so ASAP. Why pay a ridiculously high premium if you can avoid it?

Lessons Learned from the Medigap Plan N Story

The lesson of the story is to try to join a plan where most people are in the same risk category as you are. This way you will avoid surprises such as those described above. The irony of the situation is that Medicare Supplement Plan N was supposed to be a “lower utilization” plan (i.e., a plan with relatively healthy enrollees) and as such have lower premium increases. The Guaranteed Issue made it a higher utilization plan with potential high premium increases in the future.

US Government Reading

- How to Compare Medigap Policies?

- Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare

Please give us your feedback!

What do you think about Lessons learned from the Medigap Plan N story? Write your comments.

Contact Us

For help finding the best Medicare or Individual Health Plan for you, please contact Liberty Medicare or call us at 877-657-7477.

Comments are closed.