Medicare Supplement Plan D (Medigap Plan D)

UPDATED Nov. 17, 2025. Medicare Supplement Plan D, also known as Medigap Plan D, covers all Medicare ‘gaps’ except for the Medicare Part B Deductible and the Medicare Part B Excess Charges. Just as with all Medigap plans, Plan D is standardized; i.e., the benefits of the plan from one insurance company are identical to those from any other company. However, Plan D premiums will significantly vary.

Only selected Medicare Supplement insurance companies are offering Medigap Plan D.

Article Contents

When is Medigap Plan D the right choice?

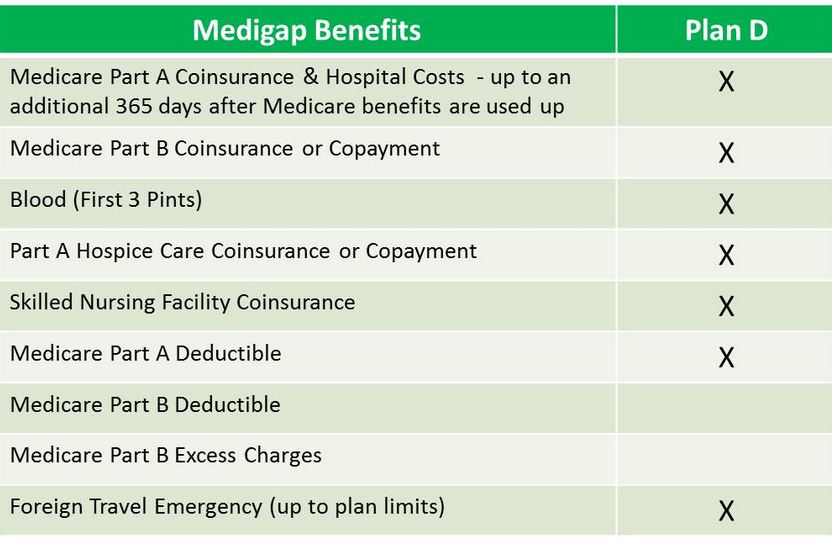

Medicare Supplement Plan D benefits include:

- Medicare Part A coinsurance – additional 365 days of hospitalization coverage.

- Medicare Part B coinsurance (usually 20% of outpatient costs) or copayment (hospital outpatient services).

- Blood: The first 3 pints of blood each year.

- Hospice Care: Coinsurance/copayment (Part A).

- Skilled Nursing coinsurance (20% that Medicare does not pay for).

- Part A Deductible – $1,736 for each benefit period in the year 2026.

- Foreign Travel Emergency

Medicare Supplement Plan D benefits do NOT include:

- Part B Deductible – $283 per year in the year 2026.

- Medicare Part B Excess Charges, which are the amounts that a doctor may charge above the Medicare-approved amount.

When is Medigap Plan D the right choice?

Medicare Supplement Plan D is identical to Medigap Plan C, with the exception that it does not cover the Medicare Part B deductible. As long as the difference between Plan C and Plan D premiums exceeds the Part B deductible, it makes the most sense to go with Plan D.

Historically, annual premium increases for Medigap Plan C are higher than those for Medicare Supplement Plan D.

Medicare Supplement Plan D is identical to Medigap Plan G, with the exception that it does not include Medicare Part B excess charges. In states where Excess Charges are illegal, such as Pennsylvania and Ohio, there is no reason to buy the more expensive Plan G; instead, Plan D will suit your needs. Since 99% of doctors accept Medicare Assignments, the need to cover Excess Charges is minimal even in States where they are acceptable.

Use Medigap Plan D (if available) when you want to save money:

- On Medigap Plan G by removing its Extra Charge coverage.

- On Medigap Plan C, when the savings in premium between Plans C and D justify removing the Medicare Part B deductible from the benefits.

As of 2020, Medicare Supplement vendors no longer sell NEW Medigap Plan C. It makes Medicare Supplement Plan D an even more attractive choice.

US Government Reading

Let Liberty Medicare Help you Choose

With 10 Standardized Medicare Supplement plans available, selecting the ideal plan becomes a challenging task. Not all Medigap providers offer all of these plans, and the premiums for the same type of plan among different vendors may vary significantly.

The experts at Liberty Medicare will work to your advantage and find the Medicare Supplement plan that is best for your needs and budget. All of our services are provided to you at no cost. Learn more about all of the benefits of working with Liberty Medicare.

We represent many well-known Medicare Supplement providers and help people save money on Medicare in the following states:

Get a free Medicare Supplement Insurance Quote, or please call us at 877-657-7477. Our specialists are ready to answer your questions.